Best High Yield Savings Accounts in Mumbai: A 2024 Guide

Your hard-earned money shouldn't just sit there. We explore the best high-yield savings accounts for Mumbaikars, turning idle cash into a growing asset.

Finding the Right High-Yield Savings Account in Mumbai

Living in Mumbai is a financial marathon. Whether you’re saving for a down payment on a flat in Panvel, planning a wedding at a banquet hall in Thane, or just trying to build a cushion against the city’s notoriously high cost of living, every single rupee counts. Yet, most of us leave a significant chunk of our cash in a standard savings account, earning a pittance in interest. It’s time we talk about a smarter, more rewarding alternative: the best high yield savings accounts available right here to us Mumbaikars. These accounts can significantly accelerate your savings goals, turning your idle cash from a lazy tenant into a hard-working employee.

What Exactly is a High-Yield Savings Account?

Let's demystify this. A high-yield savings account is exactly what it sounds like: a savings account that pays a substantially higher interest rate than a traditional one. Think about the big public sector or even some large private bank branches you see in every Mumbai neighbourhood, from Dadar to Dombivli. Their standard savings accounts typically offer interest rates hovering around a measly 2.7% to 3.5% per annum. In a city where the price of a plate of pani puri seems to inflate every six months, that’s simply not enough.

A high-yield account, often offered by digital-first banks or smaller finance banks eager to attract customers, can offer rates of 6%, 7%, or even higher. It’s not an investment in the stock market; your money isn't exposed to market risk. It's just a better savings account. The key difference is the return. It’s like choosing the Virar Fast Local over the all-stops slow train during your commute – you get to your destination (your financial goal) much, much faster.

High-Yield Savings vs. Fixed Deposits (FDs)

You might be thinking, “But my dad always told me to put money in FDs for good returns!” And he wasn’t wrong. FDs are a great tool, but they lack a crucial feature: liquidity. When you create an FD, your money is locked in for a specific tenure. Breaking it early often comes with penalties. A high-yield savings account, on the other hand, offers the best of both worlds. You get returns that can be comparable to shorter-term FDs, but with the complete freedom to withdraw your money anytime, without penalty. This makes them the undisputed champion for housing your emergency fund.

Why Your Standard Savings Account Isn's Cutting It in the MMR

Let’s be blunt. Keeping your emergency fund or short-term savings in a traditional account is like trying to fill a bucket with a hole in it. The hole is inflation. The cost of living in the Mumbai Metropolitan Region (MMR) is relentless. From your monthly rent in a Chembur high-rise to the cost of your daily commute on the new Metro lines, prices are always moving in one direction: up. The official inflation rate might be around 5-6%, but for the average Mumbaikar, it often feels higher.

Now, do the math. If your savings account is generating a 3% return and inflation is eroding your purchasing power by 6%, you are losing 3% of your money's value every single year. That ₹1,00,000 you diligently saved for a trip to Europe is effectively worth only ₹97,000 in terms of what it can buy you a year from now. It’s a silent drain on your wealth. Your money is sitting in a bank branch in Andheri, but its real-world value is slowly leaking away. This is the opportunity cost of sticking with the status quo. A high-yield account helps you fight back, earning a return that either matches or, in some cases, beats inflation.

"I advise all my clients, from seasoned investors in Colaba to young tech professionals in Airoli, to have a high-yield savings account. It’s the foundational block of a sound financial house—liquid, safe, and actually working for you against inflation."

Top Contenders: Banks Offering High-Yield Accounts to Mumbaikars

The banking landscape has changed. You're no longer limited to the handful of banks with physical branches on your street. A new wave of banks is competing aggressively for your savings, and Mumbai residents are prime targets. While specific interest rates change frequently, the players generally fall into these categories.

Digital-First & Small Finance Banks

These are the primary drivers of high-yield offerings. Banks like IDFC First Bank, AU Small Finance Bank, Equitas Small Finance Bank, and Ujjivan Small Finance Bank have made a name for themselves by offering superior interest rates. They have a growing physical presence in Mumbai and Navi Mumbai—you’ll find slick IDFC First branches in hubs like Powai and Bandra Kurla Complex (BKC), and AU Bank branches in many suburbs. However, their main strength is their robust digital platforms, allowing you to manage everything from your phone. They are aggressively seeking to grow their depositor base, and offering high interest is their main strategy.

Established Private Banks (Premium Tiers)

Don't completely write off the big guys. Banks like HDFC, ICICI, Kotak Mahindra, and Axis sometimes offer higher interest rates, but it's usually tied to their premium or 'preferred' accounts. These accounts, however, often come with very high minimum balance requirements (sometimes ₹1 lakh or more) or a total relationship value (including investments and loans). For example, Kotak Mahindra Bank's ActivMoney feature is a sweep-out facility that moves excess funds to an FD-like instrument for higher returns. If you're a high-net-worth individual who can comfortably meet these requirements, it's worth exploring the premium banking options at their flagship branches in places like Fort or Lower Parel.

Foreign Banks

Some foreign banks like DBS Bank and Standard Chartered also offer competitive rates, often through their digitally-focused products. The Digi savings account by DBS, for example, has historically offered good rates and a completely paperless account opening process. Their target audience is often the digitally savvy, urban professional working in Mumbai’s many corporate hubs.

Before you commit, it's essential to look beyond the headline number. [INTERNAL_LINK: Compare Savings Account Interest Rates]

Reading the Fine Print: What to Look for Beyond the 7% Banner

A flashy 7% interest rate banner is designed to catch your eye, but the devil is always in the details. Before you move your hard-earned savings, you need to become a savvy investigator and scrutinize the terms and conditions. Here are the critical factors to check:

- Tiered Interest Rates: This is the most common 'gotcha'. The advertised rate might not apply to your entire balance. For example, a bank might offer 3.5% on balances up to ₹1 lakh, 7% on the portion of the balance from ₹1 lakh to ₹5 lakhs, and then 6% on balances above ₹5 lakhs. You need to understand this slab structure to calculate your actual, effective interest rate.

- Minimum Balance Requirements: Many high-yield accounts are not zero-balance accounts. They may require an Average Monthly Balance (AMB) of ₹10,000, ₹25,000, or more. Failing to maintain this can result in hefty penalties that can easily wipe out your extra interest earnings. For a young professional in a PG in Vile Parle, a high AMB can be a deal-breaker.

- Account Fees and Charges: Look at the schedule of charges. What are the fees for the debit card? Are there limits on free ATM transactions? What are the NEFT/RTGS/IMPS charges? A 'free' account can become expensive if you're not careful.

- DICGC Insurance: This is non-negotiable. Ensure the bank is covered by the RBI's Deposit Insurance and Credit Guarantee Corporation (DICGC). This insures your deposits (both principal and interest) up to ₹5 lakh per person, per bank. This makes your money safe, even if the bank faces financial trouble. All commercial banks and small finance banks are covered.

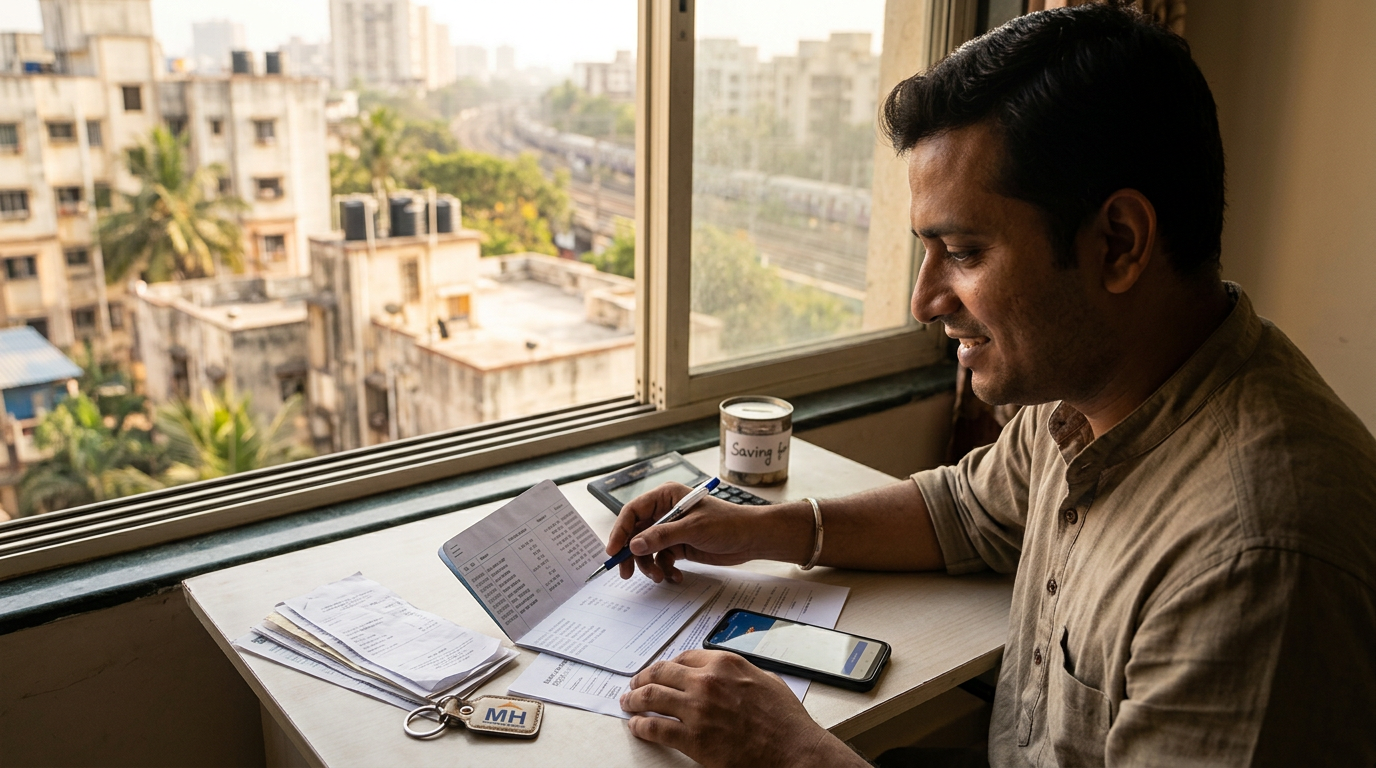

The Practical Steps: Opening Your Account from Your Flat in Kharghar

Gone are the days of taking half a day off to visit a bank branch with a file full of documents. Today, you can open a high-yield savings account while sitting in your living room in Kharghar, probably in less time than it takes for your Swiggy order to arrive. Here’s a simple, step-by-step guide:

- Research and Finalize: Based on the factors above, shortlist 2-3 banks. Visit their websites directly to see the most current interest rates, fee schedules, and account features. Don't rely on third-party aggregators alone.

- Check Your Eligibility: Most accounts require you to be an Indian resident over 18 years of age.

- Gather Your Digital Documents: You'll need your PAN card, Aadhaar card, and ensure your mobile number is linked to your Aadhaar. This is crucial for the e-KYC process.

- Start the Online Application: Go to the bank's official website or download their app. The application process is usually very intuitive. You’ll fill in your personal details, PAN, and Aadhaar number.

- Complete Your KYC: This is the magic step. Most new-age banks offer a Video KYC (V-KYC) process. You'll connect with a bank official via a video call. They'll verify your identity, ask you to show your PAN card, and take a live picture. This entire process can take just a few minutes. No more finding parking near a crowded bank branch!

- Fund Your Account: Once your account is approved (which is often instant after V-KYC), you can fund it using UPI, NEFT, or IMPS from your existing bank account. Pay attention to any initial funding requirements.

Integrating High-Yield Savings into Your Mumbai Financial Life

So you've opened your new account. Now what? The final step is to integrate it smartly into your financial system. This isn't just another account; it's a strategic tool. Here’s how to use it:

- Build Your Ultimate Emergency Fund: This is the primary use case. Calculate 6 to 12 months of your essential living expenses in Mumbai (rent, bills, groceries, transport) and build towards this target in your high-yield account. It’s liquid, safe, and it's growing.

- Power Your Short-Term Goals: Saving for a down payment on a new car to navigate the Sea Link? Planning a big solo trip? A new MacBook for your freelance work? Create specific savings 'pots' or just use the account to accumulate funds for any goal that's 1-3 years away.

- A Financial 'Parking Lot': Received a big annual bonus or sold some shares? Don't let that cash sit idle in your low-interest current account while you decide where to invest it. Park it in your high-yield account to earn solid returns in the interim. It's the perfect, productive holding bay for your money.

- Automate Your Savings: The best way to save is to make it automatic. Set up a standing instruction or recurring UPI mandate to transfer a fixed amount from your salary account to your high-yield account on the 1st of every month. Pay yourself first, before the temptations of a weekend at a mall in Malad or a dinner in Bandra can get to it. [INTERNAL_LINK: personal finance tips for beginners]

In a city that demands so much from us financially, it’s only fair that we demand more from our money. Leaving it in a traditional savings account is a missed opportunity you can no longer afford. Take an hour this weekend, do your research, and make the switch. Your future self, enjoying a bit more financial breathing room in this incredible, expensive city, will be grateful.

Keep reading

How to Save Money on Groceries: The Ultimate Mumbai Guide

Feeling the pinch from rising food costs? Our ultimate Mumbai guide reveals practical tips on how to save money on groceries, from mastering wholesale markets to decoding app discounts.

Cut Your Grocery Bill: A Mumbaikar's Guide to Saving Money

From the crowded markets of Dadar to the aisles of DMart in Panvel, grocery costs are rising. This guide offers practical, Mumbai-specific strategies to save money on groceries.

Best High Yield Savings Accounts in Mumbai (2024 Guide)

In a city where every rupee counts, your standard savings account is costing you money. We review the best high-yield savings accounts for Mumbaikars to fight inflation and grow wealth faster.